What exactly is the effect of fees on your returns and why should you be focused on keeping costs low? It all comes down to compounding.

Sure, that annual fee that your standard active fund manager charges may only seem like a drop in the ocean now, but over time, thanks to compounding, the fee looks far more significant. Think about it, every penny more paid away in fees is a penny less earning a return.

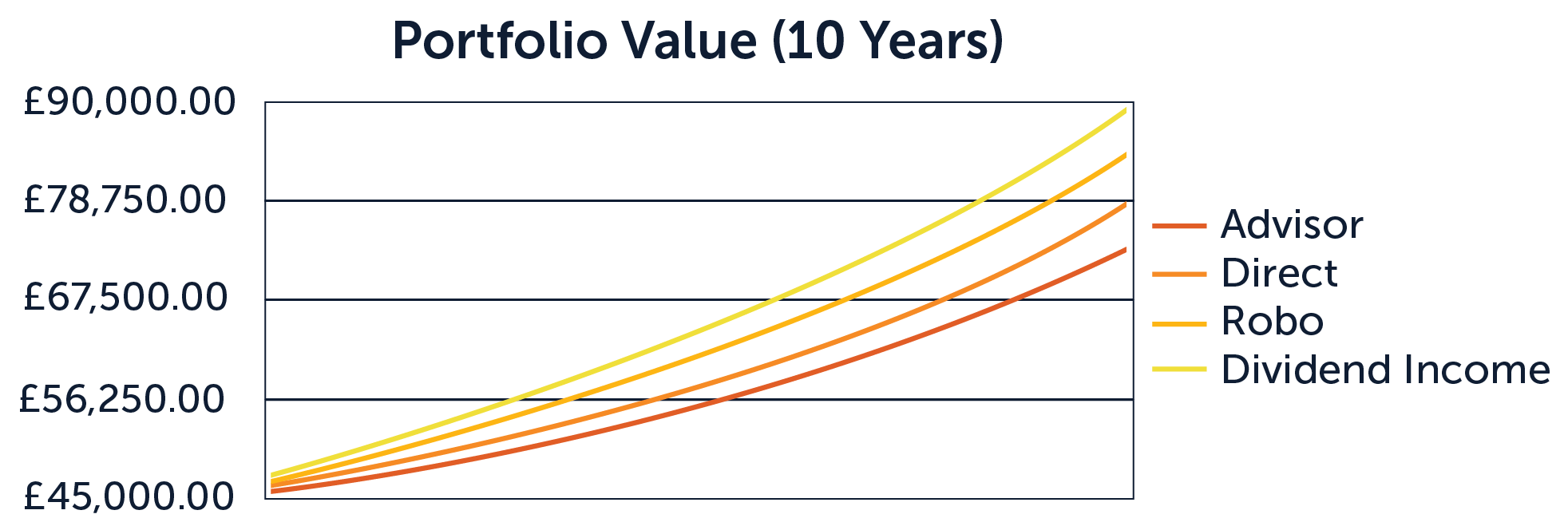

Consider the following; retail investors are primarily presented with a number of options all with differing annual on-going fees:

- Typical Financial Advisor –2.25% fee, varying initial fees.

- Direct Investment (e.g. Hargreaves Lansdown) – 1.8% fee.

- Robo Advisor (e.g. Nutmeg) – 0.94% fee.

- Investore Dividend Income – 0.5% fee.

If you invested £50,000 into the four different providers above and saw the same rate of return across them all (let’s assume 6.5% annually), the investment in the Dividend Income plan would be worth £15,360 more after ten years than the investment with the typical financial advisor. After 30 years the difference balloons further to £114,583! (Please note the return calculations are based on total returns and the Dividend Income calculation assumes all income is reinvested).

Here’s how that looks:

Investment fees vary wildly but we at investore are focused on providing our brilliantly simple solutions at one low cost. Keep more of YOUR returns and join the investore revolution today.

This article does not constitute advice. The value of your investment and the income derived from your portfolio is not guaranteed and can go down as well as up.