Dividend Income

in more detail

Brilliantly Simple!

Our investment team analyses all the shares in the FTSE100 index to select a portfolio of 20 companies that we feel will provide you with a consistent and stable dividend income.

We analyse FTSE100 companies on their on-going ability to deliver strong and growing dividends. At the same time we seek to reduce risk by ensuring the portfolio is diversified across different economic sectors.

Ultimately our approach remains focused on one brilliantly simple objective, to maintain and grow your income consistently over the long term.

It’s low cost

We have a low charging structure too.

- £150 setup charge

- Administration charge of 0.50% per annum of your initial investment

- Rebalancing cost – typically £30 per annum (based on a dealing charge of £5 per sale and purchase) but this can fluctuate depending on your portfolio. This does not apply in the first year and will never exceed £100. Elective rebalancing has a charge of £15 per sale and purchase. There is also a Stamp Duty Reserve Tax of 0.50% on all share purchases .

Example: Assuming a £10,000 investment the charges in the first year will be:

| Charge | Charge Description | Cost | Percentage of investment |

| Initial charge | Cost of setting the plan up | £150 | 1.5% |

| Administration charge | Charge made against your initial investment to pay us to manage your portfolio | £50 | 0.5% |

| Total cost in first year | £200 | 2% |

Please see our Key Information Document for more information on charges.

It works

Since the launch of the plan in April 2015 until February 2022 our investors have seen their initial investments increase in value by more than 6% per annum and received more than 4% per annum in dividend income.

So not only have they achieved capital growth but also a strong income stream that has helped provide returns above inflation over the same period.

Figures based on the Retail Price Index (RPI) as per ONS data of 3.2% annualised from April 2015 to February 2022. Past performance data is based on actual investors’ dividend income performance starting in April 2015.

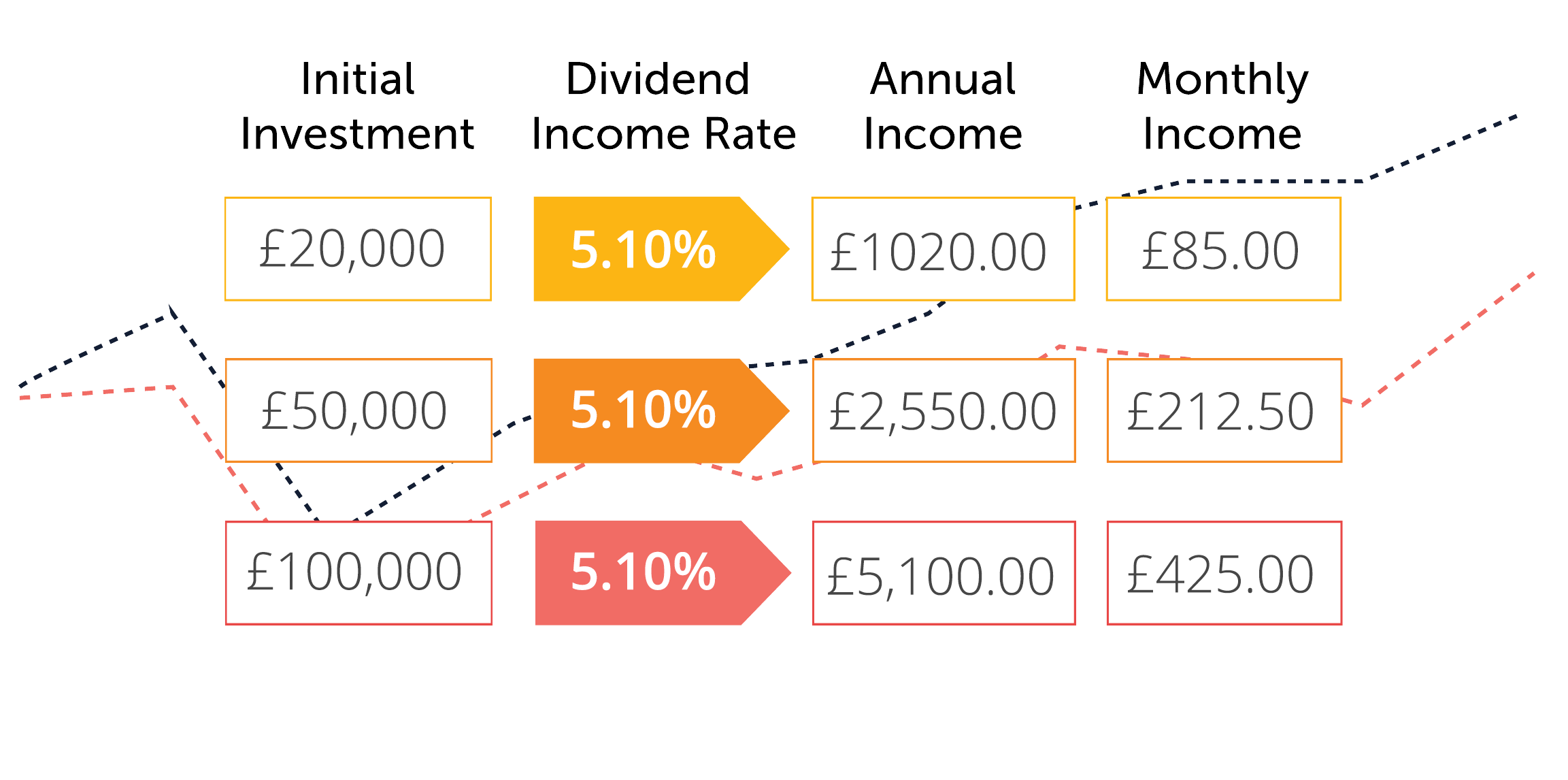

What is the effect of

the Dividend Income rate?

The figures above show what the income would be from three example investment amounts based on a 5.1% Dividend Income rate. The income you receive may be above or below this level and will fluctuate from year to year. Past performance is not a guide to future performance.

The figures above show what the income would be from three example investment amounts based on a 5.1% Dividend Income rate. The income you receive may be above or below this level and will fluctuate from year to year. Past performance is not a guide to future performance.

It’s easy to apply or transfer your current ISA

Use your ISA allowance for 2019-2020 in time for the 5th of April deadline, or by transferring your existing ISA products. You can consolidate existing ISAs into our Dividend Income Plan at any time.

FAQs

Why is yearly rebalancing of my investments needed?

Rebalancing your investments each year helps to reduce undue risk from building up in your portfolio.

Each of your individual shares will perform differently and fluctuate in value relative to each other over time. If one share performs particularly well it will eventually form a greater share of your overall value when compared to other shares in your portfolio.

This places greater emphasis on that one share from affecting the overall performance of your portfolio.

By rebalancing your plan each year we are selling some of your shares that have performed well and buying other shares that have not performed as well. This buy low sell high philosophy sounds very simple, but it will ensure that you hold a relatively equal proportion of each share in the portfolio, thus spreading your risk around a diverse number of companies and industries that make up the FTSE 100.

What are my rebalancing options?

There are two rebalancing options.

- Automatic Annual Rebalancing

This process takes place 2 weeks prior to your plan anniversary. Some shares will be sold and some will be bought in order to bring your portfolio back to an equal balance between the 20 shares. There will be no need for you to do anything, this will happen automatically unless you opt out.

- Elective Rebalancing

We also allow you to make the decision to rebalance at any time you like during the plan year. When you set your plan up, the default option is for automatic annual rebalancing.

How can I take my money out?

You can instruct an encashment any time via your online portal or by calling our customer helpline on 0330 088 4210.

We will instigate your sell request at the earliest opportunity, which will be no later than close of business the following working day. We will aim to pay the proceeds of your encashment to your nominated bank account within 5-8 working days of receiving your instruction. There will be a dealing charge of £150.

The minimum partial encashment you can make is £1,000, whilst the maximum partial encashment you can make is 75% of the value of your Plan. When making a partial encashment your remaining Plan value must be at least £5,000 following the partial encashment.

Is my money safe?

All of our clients’ money is held in a client money bank account with HSBC and protected in accordance with the FCA’s client money rules.

Once your shares have been purchased, they are held by our custodian on your behalf in accordance with the FCA’s client asset rules and you remain the beneficial owner of your investment. Your cash and investments are protected by the Financial Services Compensation Scheme which means that even if we, HSBC or our custodian went into administration you are entitled to protection.

When will I receive my first income payment?

You will receive a welcome pack no later than 5 working days after you apply. This will confirm how much income will be paid to you each month and the date you will receive your first payment. Typically the first payment is sent no later than 1 month after the initial application.

How do we calculate the Annual Rate?

The first year’s income is paid from the 5% of your initial investment that is placed into your income account at the outset of your plan. This is so we can set you up with your portfolio and collect the dividend income over the first year. The amount you receive in year one is based on the actual amount of dividends paid by the selected share portfolio over the previous year.

In year 2, your income is based on the exact amount of dividend income received into your plan over the entirety of year 1. After deducting fees, we distribute the remaining income to you in equal monthly amounts. This will be the exact same process for each of the following years you hold your plan.

The income is fixed at the start of a plan year and will be recalculated in the last month before your plan anniversary. We will contact you before the Plan anniversary to confirm your income for the following year.

Historically the income has increased over time, but this is not guaranteed. Your income may fluctuate from year to year.

How is Investore able to pay monthly when dividends are paid by companies at different times of year?

This is why we use 5% of your initial investment to fund your income in the first year. That allows us to purchase your share portfolio for you and collect the dividend income over the first year. Once this process is established we simply smooth the payments to you in equal monthly instalments from year 2 onwards.

We are simply paying you the dividend income collected by your shares in the previous year.

How do I know if a share portfolio is too risky for me?

It is important to note that at Investore we do not provide advice on the suitability of our products. Our aim is to explain the plan and make the risks as clear as possible so that you can make your own informed decision about the plans suitability for your circumstances and risk appetite.

If you are unsure about the suitability of Dividend Income please seek professional advice.

What is a corporate action?

Investopedia defines a corporate action as, “any event that brings material change to a company and affects its stakeholders, including shareholders and bondholders”

For example a merger, whereby two (or more) separate companies (e.g. Company A and Company B) combine into one larger company (Company AB), is a common form of corporate action (A + B = AB). Other common corporate actions include but are not limited to:

- Demerger: Opposite of merger. AB splits into Company A and Company B.

- Acquisition: Where one company purchases another company. Company A purchases Company B, Company A is larger while company B ceases to exist.

- Return of Capital: Situation where a company returns some of the capital invested by shareholders into the firm. The action results in a decrease in the value of the company by the amount returned and differs from a dividend in that the cash is not paid from profits for a particular period but rather the equity value on the firm’s balance sheet. An example may be when a company sells some of its long term assets (e.g. property) and returns the cash received to shareholders rather than keeping the cash on its balance sheet.

What happens if one of your shares engages in a corporate action?

Given the frequency of corporate actions, it is highly likely that one of the shares in your portfolio will undergo a corporate action at some point. Under such circumstances we will exercise a collective vote based on the direction deemed most beneficial to shareholders by the Investore Investment Committee. Investore will always seek to make the best decision for our investors as a whole but will not be held liable for any personal issues arising from applying aggregate voting requests.