The Effect of Inflation on Your Investment

What is inflation and why should you be concerned about its effect on your investments?

Inflation is officially defined as the sustained rise in the general level of prices of goods and services in the economy. On a basic level it could refer to a simple product like milk rising in price from 50p per pint in one year to 55p per pint in the next. On a more high-level basis it could refer to rising costs of living, housing and healthcare.

When considering what investment returns you require (or desire), it is essential to consider the effect of inflation. For example, someone whose day to day costs are £2,000 per month at the moment should expect them to be significantly higher in 10 years time. In fact, if the last ten years are anything to go by, living costs of £2,000 in January 2007 would have risen to nearly £2,500 in January 2017.

Another way of looking at it is to consider investment returns after factoring in inflation by considering how much an investment can buy in goods and services today compared to the future. If, for example, an investment of £1,000 was invested for a year at a 10% return, the final value after a year would be £1,100. However, if during the year the price of goods and services increased by 5%, the price adjusted or ‘real’ return would have only been 5% (the 10% return less the 5% rise in the cost of goods and services).

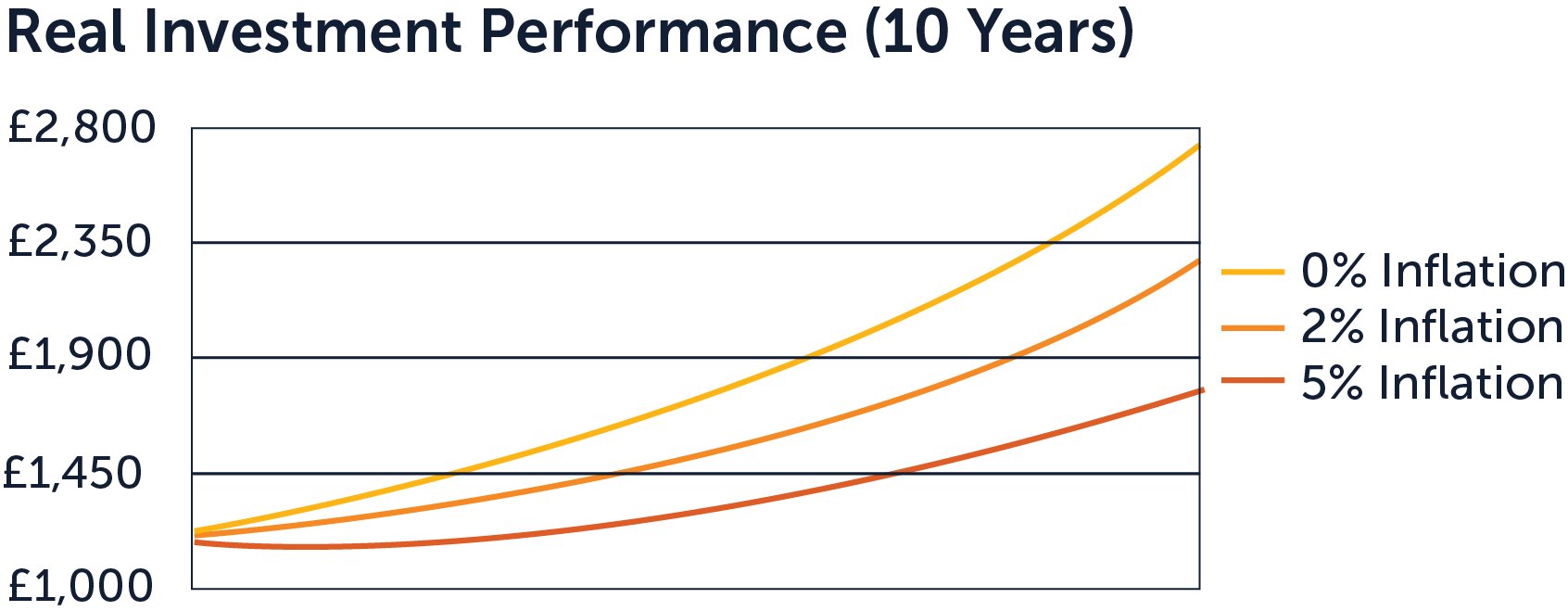

The below chart illustrates this price adjustment or ‘real’ rate of return over the long term at different rates of inflation.

Source: investore Research

As highlighted, inflation can erode returns significantly.

So how should you protect yourself?

Different asset classes provide varying degrees of protection to inflation. Equities, however, are often cited as being one of the best long term defences. Intuitively this makes sense. On a basic level, by investing in shares of companies, as the price of goods rises so to do the profits the companies earn on those goods and in turn the returns to shareholders.

The current environment of low rate cash ISA accounts and fixed savings mean millions of investors are seeing their ‘real’ investment returns turn negative. The investore dividend income plan, conversely, invests in equities and, seeks to provide long term investors with a sustainable plan to beat inflation.

This article does not constitute advice. The value of your investment and the income derived from your portfolio is not guaranteed and can go down as well as up.