As many as half of all ISA investments are made in the last three months of the tax year and, even more startlingly, 15 per cent in the final two weeks alone.

With the April 5th deadline now passed, the savvy investors will be clambering to make use of their new £20,000 ISA allowance within the first few days of the tax year and here’s why.

Your capital earns tax free returns for longer

The benefit of contributing to an ISA is that your returns are sheltered from taxation (both capital gains tax and income tax). Investing early in the year allows you to take advantage of this benefit for a longer period than investing at the end of the year.

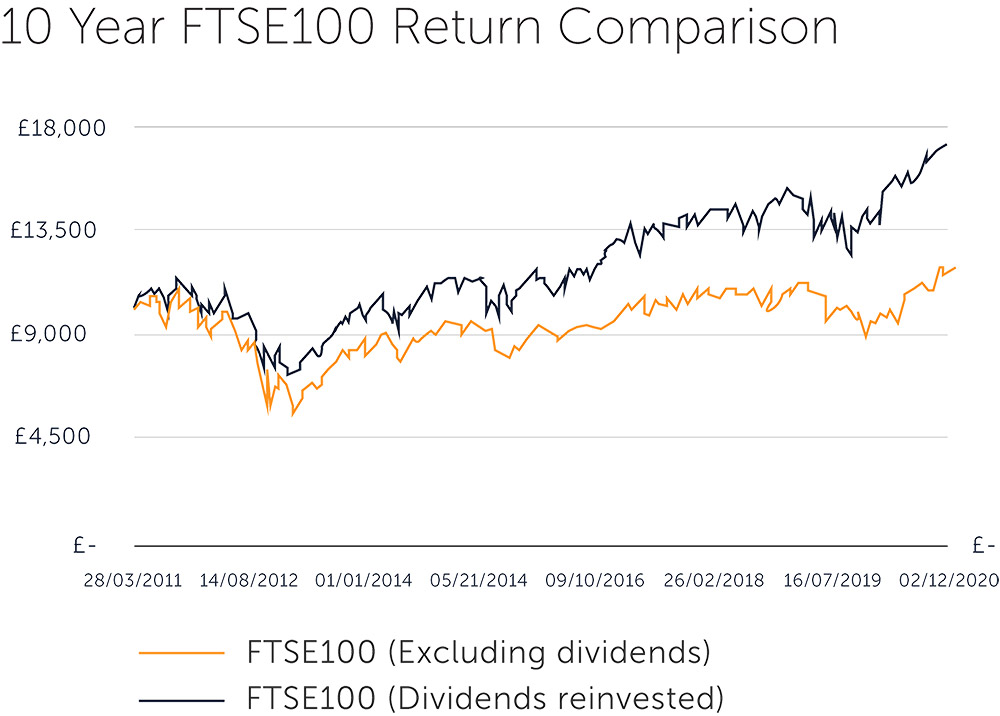

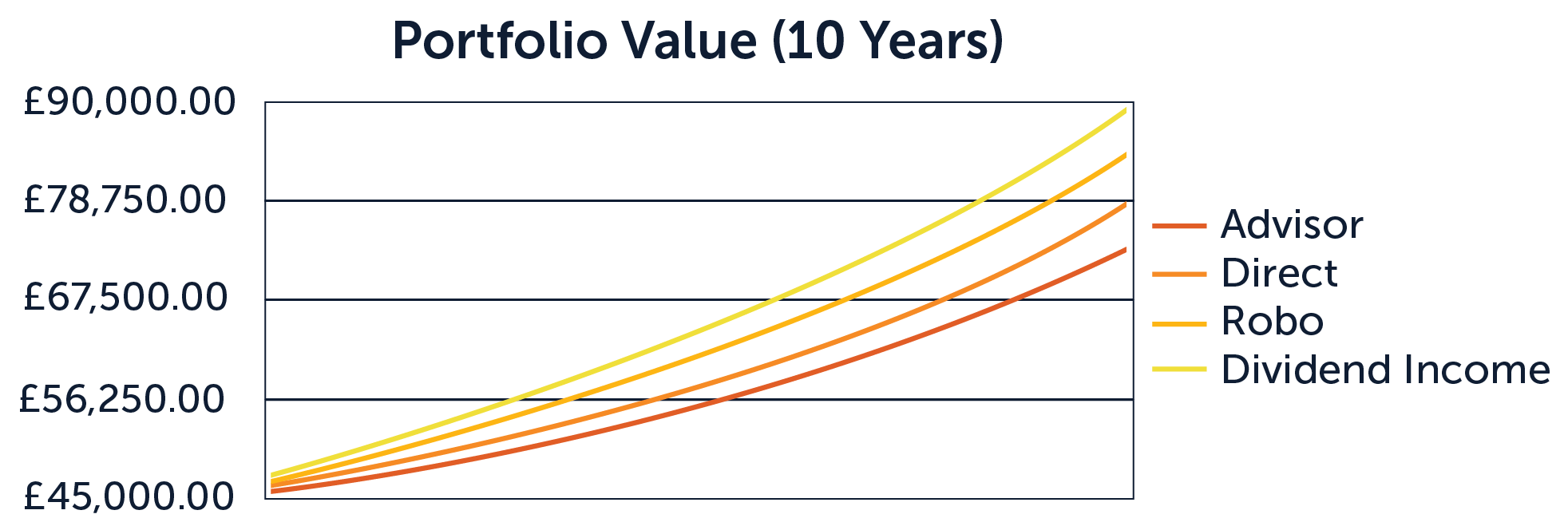

To illustrate this benefit we measured the performance someone would have seen had they invested in a FTSE100 Index Tracker over 10 years starting in the 2007/2008 tax year. More specifically, we compared the performance someone would have seen had they invested the maximum stocks and shares ISA allowance at the time on the first day of the tax year and compared that with the performance of investing the same amount on the last day of the tax year.

Source: Reuters Datastream, Investore Research, based on total returns.

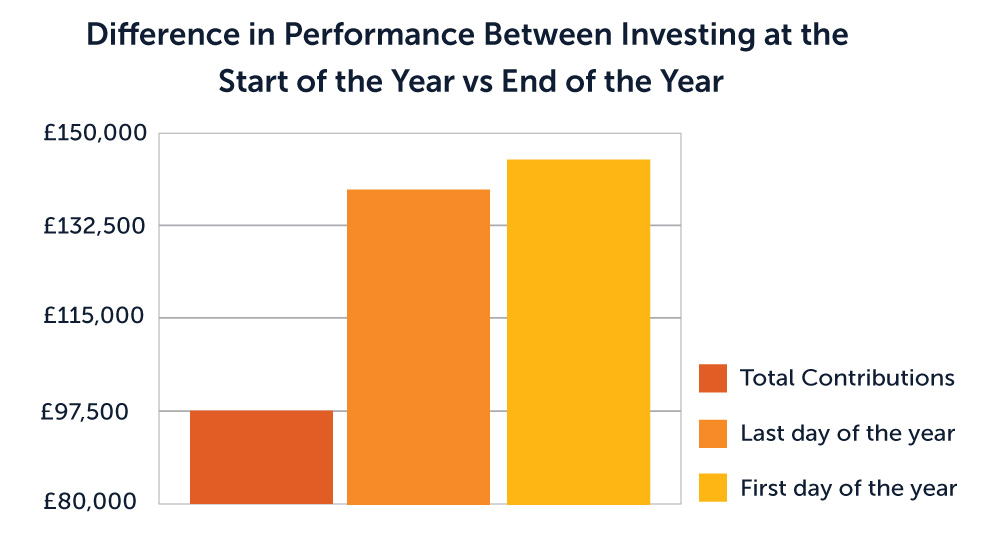

The portfolio with investments made at the beginning of the tax year would be worth approximately £7,000 more than the portfolio with the same investments made at the end of the tax year. Considering that the total contributions over the period would be £96,860, the difference equates to more than 7% of invested capital.

Of course, another benefit of investing early is the peace of mind that you’ve taken full advantage of your ISA allowance well ahead of the deadline. No rushing to get your paperwork submitted or stressing about getting you finances in order.

The Investore Dividend Income ISA application only takes about 15 minutes to complete online and not only shelters you from capital gains tax but income tax too.

This article does not constitute advice. The value of your investment and the income derived from your portfolio is not guaranteed and can go down as well as up. Taxation rules can change and any impact to you will depend on your individual circumstances.