What is a dividend?

A dividend is a sum of money that is paid out by a company to anyone that is a shareholder. Generally speaking, this dividend is based on the profits that company has made in that particular year. Even if you hold one share, you will be entitled to a dividend, if one is paid.

As an example, Company A has 100 shareholders each with one share. At the end of the year, the company has made £100 in profit. Each shareholder would then be entitled to receive £1 of that profit in the form of a dividend.

The reality is obviously far more complicated. Companies generally decide to pay out less than their profits in dividends such that they may retain some profit for the future. This can then be used to fund future investment or company growth. In other instances companies may pay out more than their profits in expectation of higher future profits.

Why dividends matter

The dividend is one of if not the primary form of return for shareholders and is a critical contributor to investment performance.

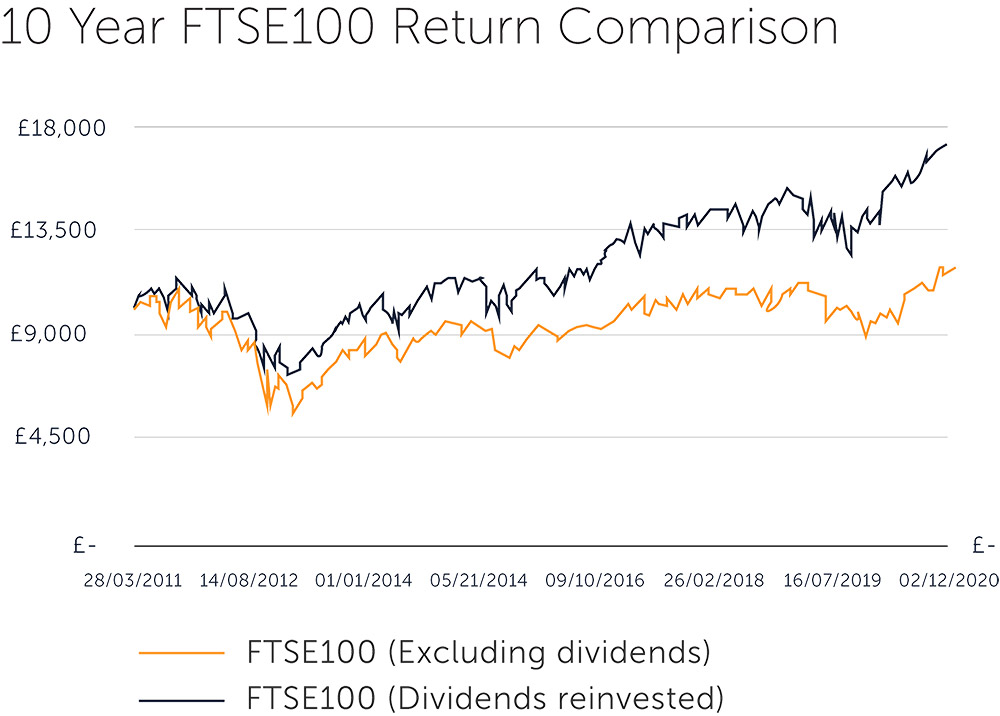

The chart below highlights the difference dividends make to total returns:

Source: ThomsonReuters Datastream, investore Research

The top line shows what an investment of £10,000 in the FTSE100 index would be worth if you consider both the change in the share prices and the dividends received. It also assumes that the dividends received are reinvested on the date of receipt (i.e. used to purchase more shares).

The bottom line, in comparison, is the change in the share prices excluding the impact of dividends. Dividends therefore contributed more than £5,200 of the total return ending the period at £16,824 compared to a less inspiring £11,591 for the index excluding dividends.

As illustrated, it is clear that dividends make a substantial difference to returns over the long run. Our Dividend Income plan looks to take advantage of this reality by providing investors with dividends even greater than those offered by the total of the FTSE100. We do this by focusing solely on the shares that are paying strong and reliable dividends.

Invest now and see the power of dividends in action.

This article does not constitute advice. The value of your investment and the income derived from your portfolio is not guaranteed and can go down as well as up.